The narrative a while back was that the world would face a shortage of heavy crude because sanctions on Iran and Venezuela had reduced production and exports. Some also implied that shale oil would fill up U.S. storage because American refiners were designed to process the heavy, high sulfur crudes from Venezuela, Saudi Arabia, and the like.

But the light, sweet crude is in high demand for export, and that appetite is likely to continue to grow with the implementation of IMO 2020 around the corner, going into effect January 1st. Freight rates from the U.S. Gulf to Europe have surged to record highs.

Equinor ASA and Unipec, the trading arm of China's top refiner Sinopec, have provisionally chartered Aframax tankers for $60,700 per day, an increase of almost 30 percent in a week, a new record high, according to shipbroker Poten & Partners. Aframax tankers are the “workhorse” of the U.S.-Europe oil trade, which has risen more than 60 percent in 2019 compared to 2018.

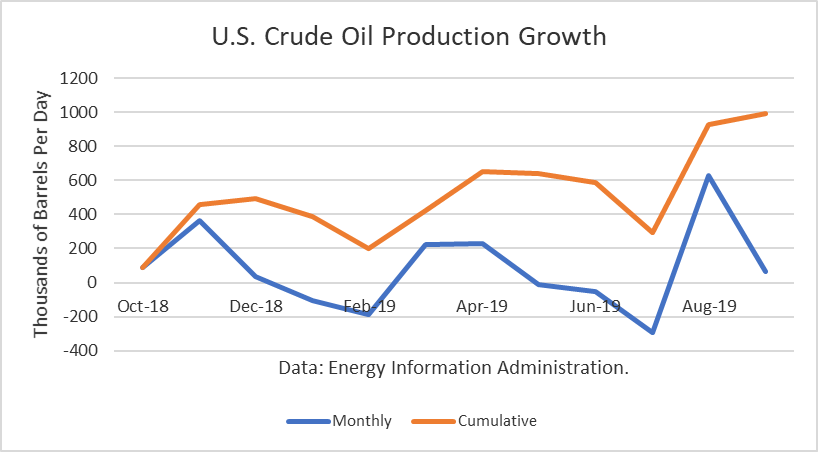

The EPIC pipeline began service in August. It has the capacity to deliver 400,000 b/d from the Permian Basin to terminals on the Gulf Coast.

The new Cactus II pipeline system also started shipping crude oil in August. It has the capacity to deliver 670,000 b/d of crude oil from the Permian.

And the Gray Oak pipeline began service in November and will be capable of delivering 900,000 b/d at capacity.

This new takeaway capacity will effectively reduce the production breakeven costs of substantial Permian crude oil because the pipeline charges are significantly lower than trucking costs.

This should provide stimulus to shale oil production growth, which had slowed due to takeaway pipeline capacity constraints. Continue reading "American Shale Oil In High Demand" →