When Donald Trump goes to Twitter Inc. (TWTR) to voice his negative opinions, investors should begin trying to find opportunities. Over just the past few weeks we have seen two separate occasions in particular in which the President of the United States has directed negative tweets at specific industries or companies. In both cases, first with Amazon.com Inc. (AMZN) and more recently with The Organization of Petroleum Exporting Countries (OPEC), his tweets have sent asset prices lower for a short period, before they have recovered, opening up big opportunities for investors.

Amazon

The end of March, beginning of April, Donald Trump assaulted Amazon with some tweets. First, it was that the company paid little to no state and local government taxes and then it was that the e-commerce company was a ‘scam’ which costs the US Post Office and therefore the American people, billions of dollars a year. Another string of tweets pointed the finger at Amazon claiming it was the reason thousands of retailers were going out of business, and millions of US workers had been laid off.

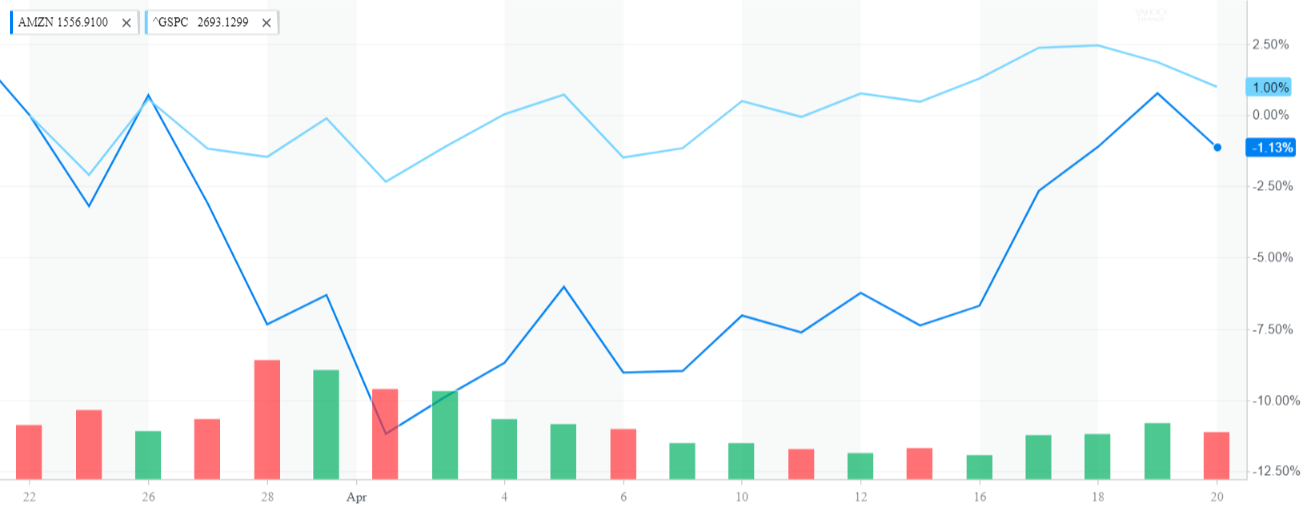

The tweets from Trump sent Amazon shares lower each day he would reignite his attack on the e-commerce giant. A 1-month chart of Amazon shows how the stock fell during the Presidents attacks and has since recovered.

From Yahoo Finance

Despite the fact that the President attacked Amazon and no real solution has come from the issues he pointed out, Amazon’s recovery appears to be nearly complete. This is not to say that the problems with Amazon not paying taxes or its contract with the Post Office couldn’t be reignited again in the future. But as most analysts have noted, the Presidents threats and claims against Amazon have no real teeth. Continue reading "Trump Tweets Create Opportunity for Investors"