A lot, if not everything, in the world of finance, is based on trust: trust that the future would be better than the present; trust that a dollar bill would guarantee an equivalent worth of goods and services at a given point in time; and trust that wealth created would be safe, accessible, and transferable at all times.

So, when events like those unfolding over the past fortnight undermine one or more of the aforementioned collective beliefs, the ensuing risks can quickly become systemic and existential.

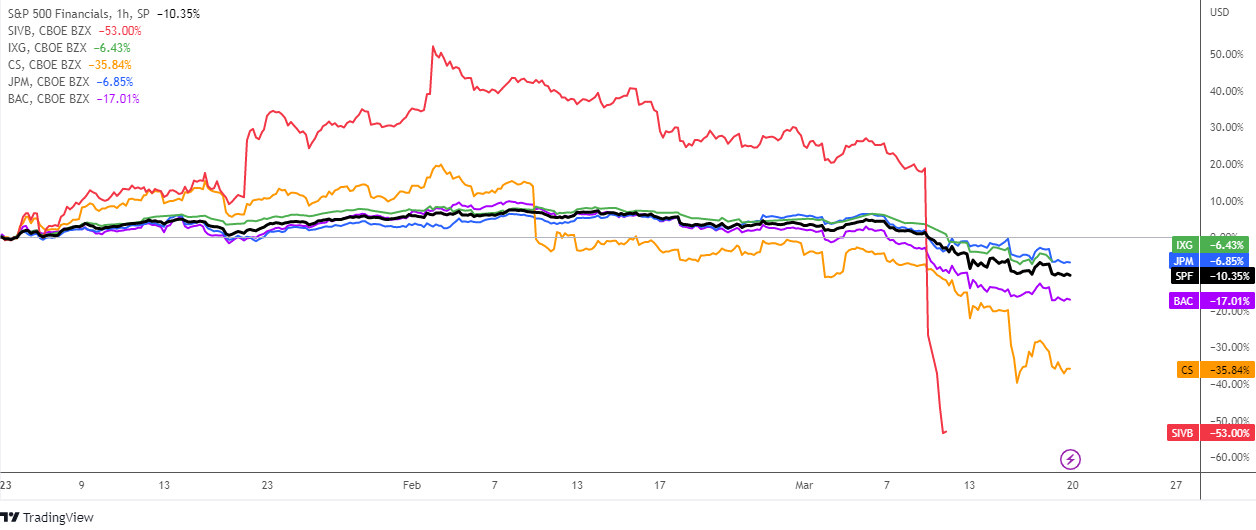

On February 24, KPMG signed an audit report giving SVB Financial, Silicon Valley Bank’s parent company, a clean bill of health for 2022.

On March 10, federal regulators announced that they had taken control of the bank, which reopened the following Monday as Deposit Insurance National Bank of Santa Clara.

This was the second-biggest bank failure since Washington Mutual’s collapse during the height of the 2008 financial crisis. It was soon followed by the third-biggest, with Signature Bank shuttered by the regulators to stem the fallout from Silicon Valley Bank’s failure.

The resulting crisis of confidence has somehow been contained with an assurance that all insured and uninsured depositors would get their money back, the announcement of a new lending program for banks, and 11 banks depositing $30 billion in the First Republic bank.

However, the contagion risk subsided only after claiming an illustrious victim from the other side of the Atlantic, with UBS agreeing to take over its troubled rival Credit Suisse for more than $3 billion in a deal engineered by Swiss regulators.

Since we are more or less up to speed, let’s look deeper into what can make banks seem unbankable in a little over two weeks. Continue reading "Why Banks Fail"