The 173rd OPEC Meeting and 3rd non-OPEC Ministerial Meeting concluded with an agreement to extend the production cuts all the way through 2018. Saudi minister Khalid Al-Falih also implied that production in 2018 by Nigeria and Libya would not increase, based on information from those countries. In 2017, large increases by the pair undermined cuts made by others.

The official OPEC press release included two caveats, though not unusual but were obviously a concession to Russia, that the deals could be modified, depending on market conditions:

"In view of the uncertainties associated mainly with supply and, to some extent, demand growth it is intended that in June 2018, the opportunity of further adjustment actions will be considered based on prevailing market conditions and the progress achieved towards re-balancing of the oil market at that time."

"To support the extension of the mandate of the Joint Ministerial Monitoring Committee (JMMC) composed of Algeria, Kuwait, Venezuela, Saudi Arabia and two participating non-OPEC countries of the Russian Federation and Oman, chaired by Saudi Arabia, co-chaired by the Russian Federation, and assisted by the Joint Technical Committee at the OPEC Secretariat, to closely review the status of and conformity with the Declaration of Cooperation and report to the OPEC – non OPEC Conference."

Initially, at the meeting a year ago, the oil ministers predicted that the glut would disappear within six months. Then at the May meeting, the Saudi minister predicted that the extension would "do the trick" of draining the glut "within six months."

By intervening in the oil market for a second year, Saudi Arabia backed a strategy Mr. Al-Falih had previously said would not work. In March 2017, he stated during a conference in Houston:

"…History has also demonstrated that intervention in response to structural shifts is largely ineffective, and I believe we've learned that lesson. That's why Saudi Arabia does not support OPEC intervening to alleviate the impacts of long-term structural imbalances, as opposed to addressing short-term aberrations such as financial crises, economic recessions, unforeseen supply disruptions, or the like."

Leading up to this meeting, Mr. Al-Falih admitted that the glut would continue through March 2018, the end of the extension set in May. In the press conference following the meeting today, he stated that the market is entering the seasonally soft (demand) time of the year, and inventories may even increase.

What he did not admit is that global OECD stocks may be just as large at end-December 2017 as they were at end December 2016, right before the deals went into effect. The OPEC goal is to reduce those stocks to their five-year average.

Originally, at the November 2014 meeting, OPEC adopted a strategy designed to flood the market to put shale oil producers out-of-business. When that didn’t work, they shifted to the cuts as a means for reducing inventories.

What they did not count on was a rapid response by American shale oil producers, who began raising production as OPEC and the others were reducing their output. A year ago, Mr. Al-Falih said he did not expect any response by shale oil in 2017.

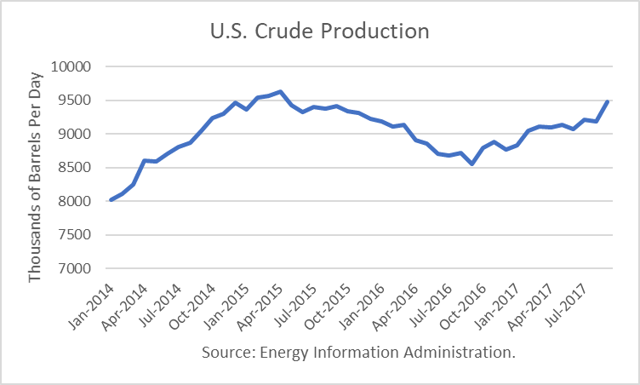

Unscheduled maintenance in the Gulf of Mexico (GOM) affected U.S. production beginning in April, and so US output growth slowed, misleading some market observers. In fact, Mr. Al-Falih remarked during today’s press conference that the fears about shale oil production growth were overblown and that strong growth has not materialized as expected.

Ironically, the DOE reported today, during OPEC’s deliberations, that September production rose by 290,000 b/d from August, a very large increase to 9.481 million barrels per day (mmbd). Hurricane Nate reduced GOM production by an estimated 8.4 million barrels, or 271, 000 b/d over October. And so the November report (due out late January) will likely deliver another huge one-month gain then.

Conclusions

If the DOE projections for 2018 prove to be correct, global OECD stocks will be higher at end-2018 than at either end-2016 or end-2017. If that is the case, the deals will most likely end in failure.

But the sailing will not be smooth in the meantime. Weak demand in 1Q18 will likely push stocks higher, increasing the glut. The bullish sentiment that gathered steam in the last few months is likely to wither, and high speculative long positions are likely to be gutted as traders exit, putting downward pressure on prices once again.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor - Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.