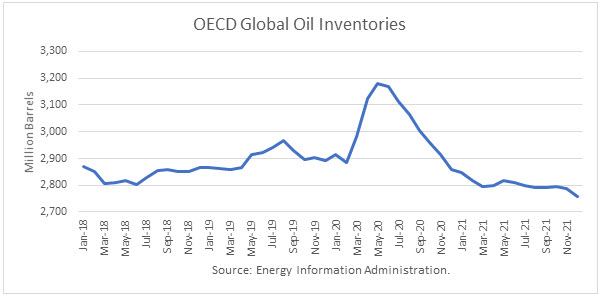

The Energy Information Administration released its Short-Term Energy Outlook for August, and it shows that OECD oil inventories likely bottomed in this cycle in June 2018 at 2.804 billion barrels. It estimated stocks dropped by 58 million barrels in July to end at 3.113 billion, 172 million barrels higher than a year ago. It estimates that inventories peaked in May 2020 at 3.181 billion.

The EIA estimated global oil production at 88.72 million barrels per day (mmbd) for July, compared to global oil consumption of 93.42 mmbd. That implies an undersupply of 4.69 mmbd or 146 million barrels for the month. About 88 million barrels of the draw for July is attributable to non-OECD stocks.

For 2020, OECD inventories are now projected to draw by a net 34 million barrels to 2.859 billion. For 2021 it forecasts that stocks will draw by 102 million barrels to end the year at 2.757 billion.

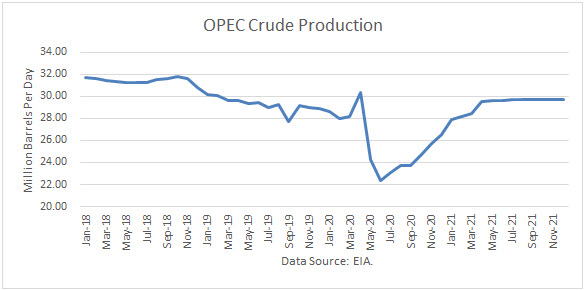

The EIA forecast was made to incorporate the OPEC+ decision to cut production and exports. According to OPEC’s press release:

“Adjust downwards their overall crude oil production by 9.7 mb/d, starting on 1 May 2020, for an initial period of two months that concludes on 30 June 2020. For the subsequent period of 6 months, from 1 July 2020 to 31 December 2020, the total adjustment agreed will be 7.7 mb/d. It will be followed by a 5.8 mb/d adjustment for a period of 16 months, from 1 January 2021 to 30 April 2022. The baseline for the calculation of the adjustments is the oil production of October 2018, except for the Kingdom of Saudi Arabia and The Russian Federation, both with the same baseline level of 11.0 mb/d. The agreement will be valid until 30 April 2022, however, the extension of this agreement will be reviewed during December 2021.”

Oil Price Implications

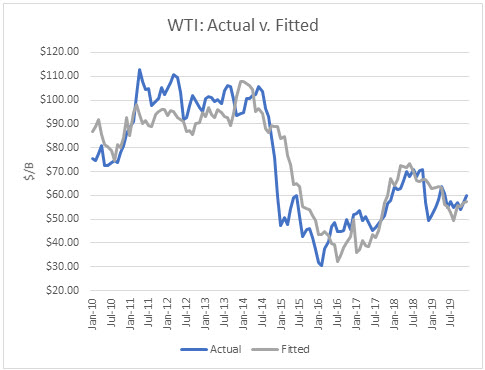

I updated my linear regression between OECD oil inventories and WTI crude oil prices for the period 2010 through 2019. As expected, there are periods where the price deviates greatly from the regression model. But overall, the model provides a reasonably high r-square result of 79 percent.

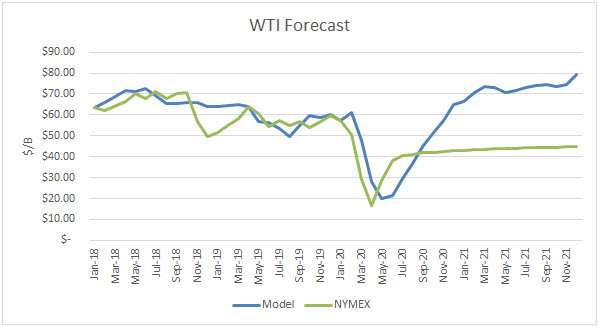

I used the model to assess WTI oil prices for the EIA forecast period through 2020 and 2021 and compared the regression equation forecast to actual NYMEX futures prices as of August 10th. The result is that oil futures prices are presently overvalued through August 2020. However, futures prices are undervalued starting in October 2020 through the forecast horizon in 2021. This represents a major change to the forecast, which previously had prices overvalued for much of the forecast period beginning in December.

Uncertainties

April 2020 proved that oil prices can move dramatically based on expectations and that they can drop far below the model’s valuations. In contrast, prices in May through July proved that market factors in future expectations beyond current inventory levels.

The most important uncertainty is how deeply and how long the coronavirus will disrupt the U.S. economy. The U.S. has become the epi-center of the pandemic and is the largest economy and oil consumer in the world. Efforts to open the economy back up have resulted in a surge of new cases of the virus. Therefore, some major states, such as Texas and California, have had to roll back reopening plans.

It is also unknown how much, if any, of the demand destruction will be permanent due to changes in business, such as online meetings instead of face-to-face meetings, work-at-home, and concerns about flying with infected people.

Changes in supply are almost equally uncertain, but producers’ behavior have become somewhat clearer. OPEC members did follow-though overall with cuts and have most recently signaled that the cutbacks will be reduced so as not to push oil prices too high, which would only incentivize production from non-OPEC sources, such as shale oil.

U.S. oil production was almost two million barrels a day lower than the EIA had been forecasting and reporting in its weekly data. And so EIA forecasts of forward U.S. production should not be viewed as reliable at this point.

Another major unknown is if a “second wave” of the virus will return in the second half of the year, as is being predicted by some scientists. Also, unknown is when effective treatments will be developed and manufactured so that health threats can be mitigated, and if and when a safe and effective vaccine will be developed and how long immunity may last after a person recovers from an infection.

Conclusions

This pandemic is the biggest market-moving event in the modern history of the oil market. And given its uniqueness, there is no reliable way to know how it will unfold. The public’s willingness and capacity to tolerate measures designed to mitigate the spread of the virus, including a large group of thirty to fifty percent of the population who would not trust the safety of a new vaccine.

For now, the WTI futures price of around $40/bbl seems to be at the top end of the trading range. But the EIA’s August inventory forecast implies oil prices may double by the end of 2021, based on their supply/demand forecasts.

Check back to see my next post!

Best,

Robert Boslego

INO.com Contributor - Energies

Disclosure: This contributor does not own any stocks mentioned in this article. This article is the opinion of the contributor themselves. The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. This contributor is not receiving compensation (other than from INO.com) for their opinion.