It was another turbulent week for the major averages, with the S&P 500 (SPY) finding itself down 3%, extending its decline to the 20% mark. However, one sanctuary from the turbulence was the Gold Miners Index (GDX). Not only did the index not lose ground last week, but it gained 3%, and it is one of the few ETFs sporting a year-to-date gain. This continued relative strength combined with an undervalued industry group relative to historical levels suggests that this is a group worth keeping a close eye on for investors looking to inflation-proof their portfolios.

With inflation readings continuing to sit at multi-decade highs and the Federal Reserve maintaining its hawkish pivot, there are few places to hide in today's market. However, one asset that has historically done well in periods of negative real rates is gold (GLD), and one way to collect income with exposure to the gold price is through gold miners. The caveat, however, is that they must be trading at a deep discount to net asset value [NAV] and ideally out of favor. With more than 80% of miners trading at discounts to NAV and the industry group down nearly 40% from its Q3 2020 highs, it currently meets both requirements. Let's look at three names that make for solid buy-the-dip candidates:

B2Gold (BTG)

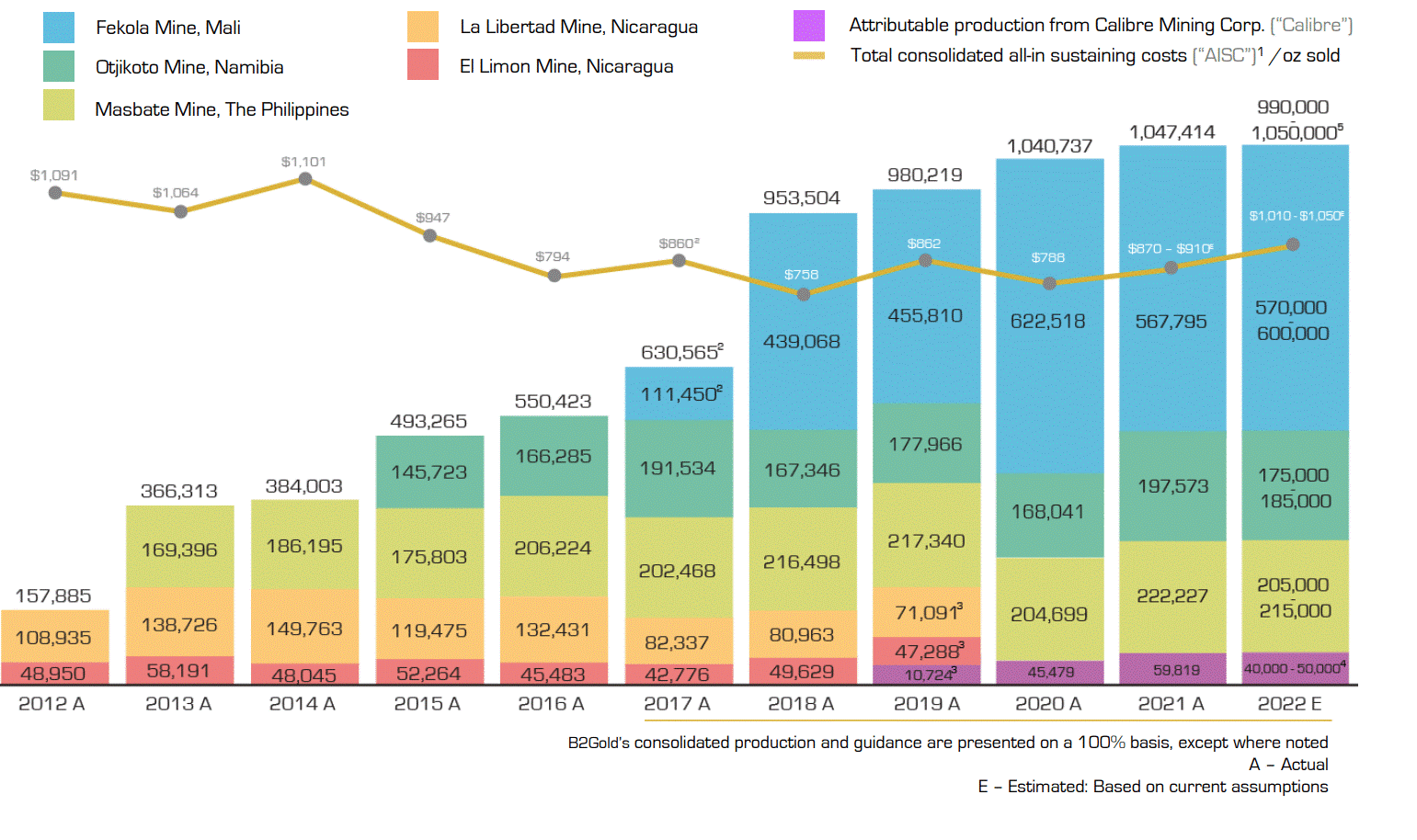

The first name worth highlighting for investors looking for gold exposure is B2Gold (BTG), a million-ounce gold producer with mines in Mali, Namibia, and the Philippines. Usually, I tend to avoid companies that lack exposure to the safest mining jurisdictions (Canada, USA, Finland, Australia). Still, in the case of B2Gold, the company is too consistent and well-run to ignore. In fact, the company has an industry-leading growth rate, one of the best margin profiles sector-wide, and has beaten guidance for several years in a row. Given this consistency, B2Gold stands head & shoulders above many of its mid-cap peers.

B2Gold has underperformed its peers from a return standpoint over the past 18 months, but this is largely due to being up against difficult comparisons after growing its production by more than 500% in 10 years. This figure dwarfed the industry average, but with the company seeing peak earnings in 2020 ($0.50 per share) and near-peak production, investors moved to greener pastures. However, after a massive upgrade to its Malian resource base, the company is now gearing up for more growth, looking out to 2026, with the potential to increase production to 1.3+ million ounces (~30% growth). Notably, BTG has two options for this growth, including constructing a new mine in Colombia or adding a second operation in Mali 20 kilometers north of its current Fekola Mine.

Assuming the company can execute on this growth, we should see annual EPS increase to $0.60 in FY2026, which assumes no help from the gold price. This would leave BTG trading at less than 6.7x earnings, or just 5.8x earnings if we subtract out net cash of $0.65 per share. Meanwhile, investors are getting a 4.0% yield ($0.16 annualized dividend) while waiting for this growth. So, for long-term investors looking to hedge against inflation while collecting income with a margin of safety, BTG is an excellent pick.

Royal Gold (RGLD)

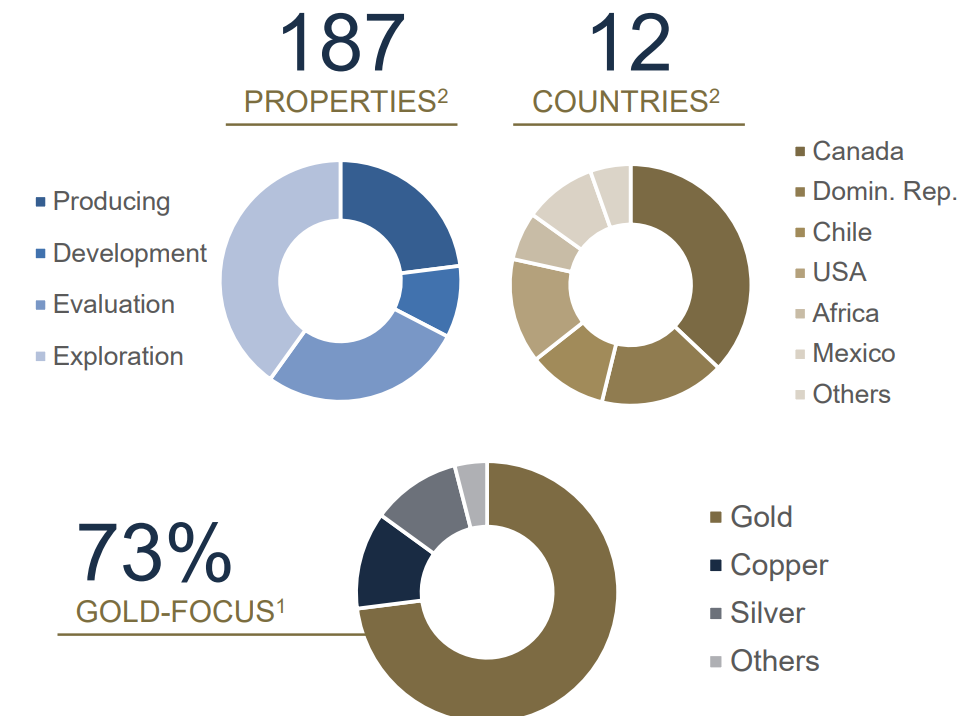

When it comes to getting exposure to the gold price with the least amount of risk possible, Royal Gold (RGLD) is one name that does the job. For those unfamiliar, the company is one of the top-3 largest precious metals royalty and streaming companies globally, sporting a market cap of $8.0BB and annual revenue of ~$650MM. While this may seem like a very steep valuation (12x sales) for a cyclical company, Royal Gold has some of the highest margins sector-wide (~83%) due to its business model, which involves collecting recurring revenue from a portion of production from multiple mines globally in exchange for its already paid-for upfront payments (187 total properties in 12 countries with 43 assets already producing).

Based on RGLD's 2022 guidance, the company expects to report sales of up to 340,000 gold-equivalent ounces [GEOs], translating to revenue of just over $650MM, assuming a $1,900/oz average realized gold price. However, the company has a very solid organic growth profile with more than a dozen of its operations either in construction, in expansion, or soon to begin construction. This should propel RGLD's revenue to more than $840MM in 2026, translating to a very respectable growth rate for a company of its size. Based on what I believe to be a fair revenue multiple of 15 and 66MM shares outstanding, this translates to a fair value north of $190 per share for its 3-year target price.

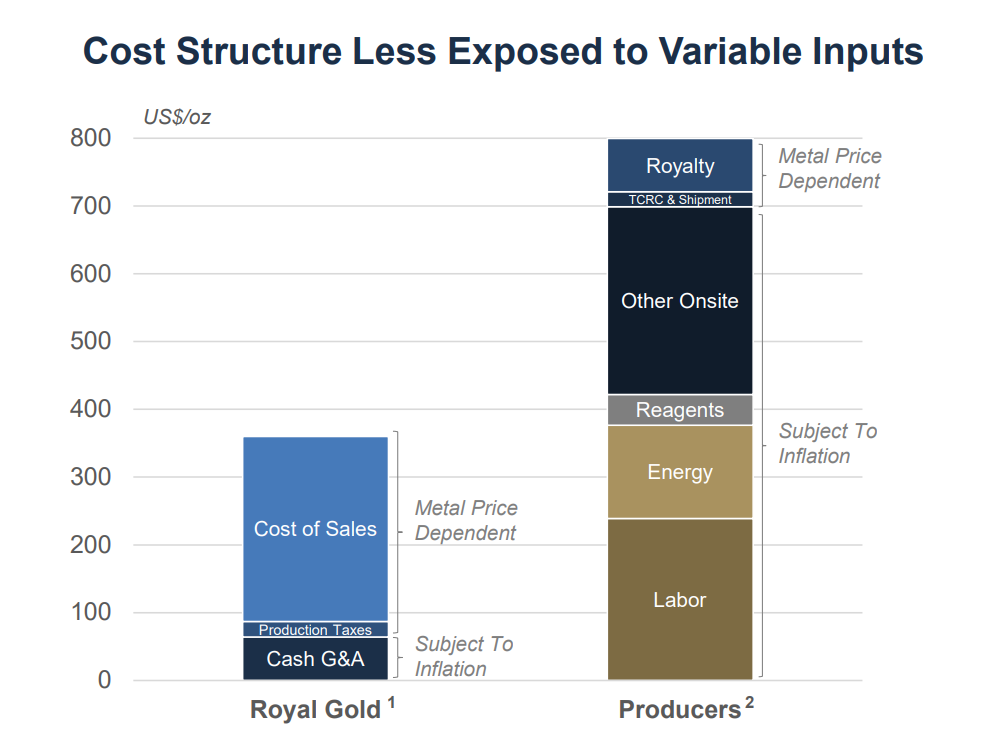

While some investors might be looking for more than 65% upside to a 3-year forward target price, it's important to note that RGLD has one of the best risk profiles, given that only its G&A is subject to inflation vs. inflation on labor, energy, consumables, and other on-site costs for producers. Hence, while I see a 65% upside to its 3-year fair value, I see only a 12% downside, giving RGLD one of the best reward/risk profiles sector-wide.

Kinross Gold (KGC)

The last name worthy of investment is Kinross Gold (KGC), a 2.1-million-ounce gold producer with mines in the United States, South America, and Mauritania. Unfortunately, while Kinross came into the year armed with a solid growth profile and being undervalued, the Russian invasion of Ukraine has complicated matters, with Kinross deciding to divest its Russian mine (Kupol) and its Russian development project (Udinsk) for ~$800MM. These two projects represented approximately 15% of total gold production, which has shifted Kinross from a growth story to a no-growth story.

While this isn't ideal, the stock is now selling for a ~16% FY2023 free cash flow yield, paying a nearly 3.0% dividend yield, and having a very low payout ratio below 50%, suggesting its yield is secure. Meanwhile, the company recently acquired what looks like it could be one of the top-15 gold mines globally (among over 200 operations). This Canadian project (Dixie) has the potential to produce over 450,000 ounces per year at sub $750/oz costs in 2028. This would return KGC to growth at higher margins and lead to multiple expansion (a higher P/NAV ratio), though investors will have to wait for this growth. So, while I would normally avoid a no-growth story, KGC is too cheap to ignore for investors willing to be patient. Hence, I see this pullback below $4.40 as a buying opportunity.

Taylor Dart

INO.com Contributor

Disclosure: This contributor held a long position in KGC at the time this blog post was published. This article is the opinion of the contributor themselves. Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information in this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying small-cap precious metals stocks, position sizes should be limited to 5% or less of one's portfolio.