It’s been a rollercoaster ride for investors in the Gold Miners Index (GDX), with the index starting the year up 24% only to find itself back at a negative year-to-date return. While this has led to disappointment among many investors, I believe that this complete retracement is a gift, and it's worth noting that the GDX is still massively outperforming other sectors despite the sharp reversal. However, the key when investing in gold miners is to buy quality, and it rarely pays to bet on turnarounds from the lower-quality or lower-priced names in hopes that they will play catch-up. In this update, we'll look at three sector leaders worthy of a closer look.

Agnico Eagle Mines (AEM), Eldorado Gold (EGO), and Maverix Metals (MMX) all provide exposure to the gold price but have little in common from a cost, scale, and jurisdictional standpoint. All three operate in very different jurisdictions and have costs ranging from $400/oz to $1,300/oz. From a size standpoint, Maverix produces as little as ~40,000 gold-equivalent ounces [GEOs] per annum on an attributable basis. In contrast, Eldorado Gold produces over 400,000 GEOs per year, and Agnico produces over 3 million ounces of gold each year. However, all three companies share one key trait: enviable organic growth. In a sector that lacks growth stories, with most being inorganic, these companies do not need a higher gold price to significantly increase cash flow per share looking out to FY2025.

Beginning with Agnico Eagle Mines (AEM), the company is the 3rd largest gold producer globally and expects to produce 3.3 million ounces of gold in 2022 at all-in sustaining costs [AISC] between $1,000/oz to $1,050/oz. The company's 10+ mines are located in Canada, Australia, Finland, and Mexico, and the company has a large development that could add 700,000+ ounces per annum of production by 2030. Among the million-ounce producers, this jurisdictional safety is a rarity and is one reason that AEM is a favorite among funds, with 95% of production coming from Tier-1 ranked jurisdictions vs. Barrick Gold and Newmont at less than 60%, and Gold Fields at less than 50%.

While Agnico's jurisdictional profile separates it from its peers and makes it a low-risk way to get exposure to the gold price, it's the growth profile that should excite investors the most. This is because, within the portfolio, Agnico has a path to 4.3 million ounces of production per annum by 2030, with an upside case of 4.5 million ounces. Assuming the company can deliver on this growth, this would translate to upwards of 30% production growth at the mid-point (4.4 million ounces), while its peers NEM, GOLD, and GFI will see less than 5% production growth in the same period. In my view, this should translate to a premium multiple, but as it stands, AEM trades at a discount to its peers.

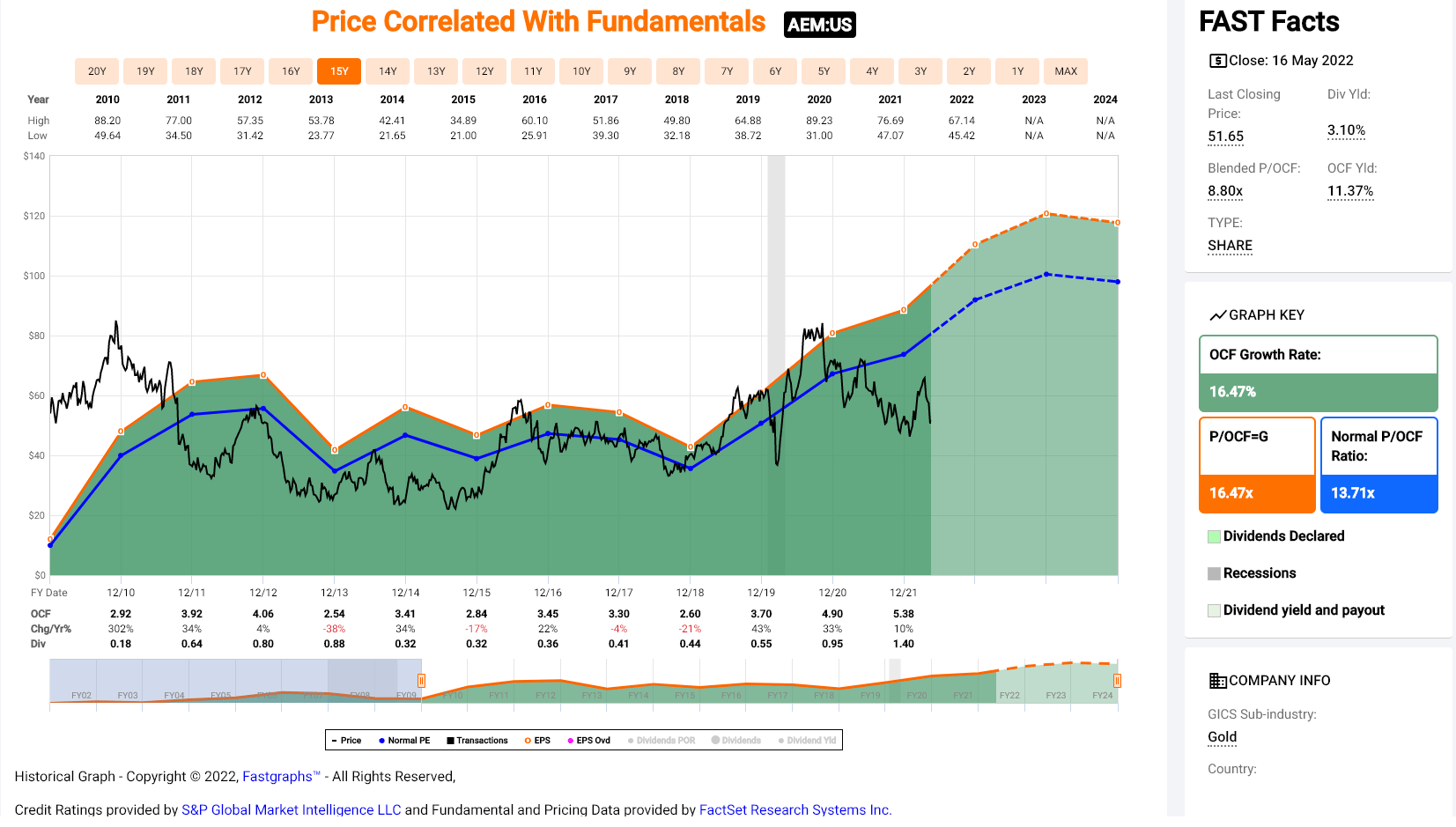

The chart above shows that AEM has historically traded at 13.7x cash flow and currently trades at less than 9x FY2023 cash flow estimates ($6.00 per share). This leaves the stock trading more than 30% below fair value. However, this does not give any upside for the company's development portfolio (non-operating), which could generate upwards of $1.4BB in annual revenue in FY2030. Given this deep discount to fair value, I see this pullback in AEM as a buying opportunity, and I have recently added to my position. In addition to the significant upside, if the stock trades up to fair value ($78.00 per share), investors can pick up a 3.1% dividend yield at current prices, a bonus to the investment thesis.

The second miners name worth highlighting is Eldorado Gold (EGO), a mid-tier gold producer operating in Greece, Turkey, and Canada. In 2022, the company is targeting the production of ~475,000 ounces of gold at sub $1,200/oz costs, with the bulk coming from its Lamaque Mine in Canada and its Kisladag Mine in Turkey. While this is a respectable production profile, it's well below the ~529,000 ounces of gold produced in FY2020, and the stock came out of the gate weak with soft Q1 results, leading to a sharp sell-off in the stock.

The weak Q1 production was related to COVID-19-related absenteeism and was out of the company's control, and while the ~93,000 ounces produced was disappointing, the company has maintained its 460,000 to 490,000 guidance outlook. However, while the market seems to be focused on the short-term, this view is missing the forest for the trees. In terms of the big picture, EGO is the proud owner of the Skouries Project in Greece, which could produce more than 300,000 GEOs per annum at costs below $100/oz. This would make it one of the lowest-cost mines globally, transforming EGO from a 480,000-ounce producer with $1,200/oz costs to an 800,000-ounce producer with sub $900/oz costs, translating to a significant re-rating. Hence, with the market focused on the mediocre Q1 results, I think investors are getting a great buying opportunity on EGO for a starter position below US$8.50.

The final name on the list is Maverix Metals (MMX), a junior royalty company that has grown its production profile from ~20,900 GEOs in FY2018 to 32,000 GEOs in FY2021. For those unfamiliar, royalty companies are one of the safest ways to play the gold space, given that they provide upfront capital to producers and developers in exchange for a portion of the life of mine production from a given asset. This allows them to participate in the asset's upside and gain exposure without the adverse effects of inflation on operating costs and sustaining/expansion capital.

While Maverix's growth has been strong to date, its organic growth is also impressive, with the company set up to grow attributable production to 50,000+ GEOs by FY2026 if it can execute successfully. This would translate to revenue of nearly $95MM per annum and easily justify a market cap of $1.14BB, or 12x sales, or a share price of US$7.88 based on 145MM shares outstanding. This represents more than 85% upside from current levels, making MMX one of the most undervalued royalty names. Hence, I would view any pullbacks below $4.20 near support as buying opportunities.

While the gold sector can be difficult to invest in, given the number of laggards with mediocre leadership, MMX, AEM, and EGO are three ways to play the sector with significant upside that do not rely on a higher gold price. Hence, I see the current pullback in these miners as a buying opportunity.

Taylor Dart

INO.com Contributor

Disclosure: This contributor held a long positions in AEM, NEM, and GLD at the time this blog post was published. This article is the opinion of the contributor themselves. Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information in this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying small-cap precious metals stocks, position sizes should be limited to 5% or less of one's portfolio.