The most valuable resource in a mining company is often the people. Good management can attract the right investors and add value regardless of the market. In this interview with The Gold Report, Marin Katusa, founder of Katusa Research, shares his litmus test for which mining companies are worth his hard-won dollars and which ones he is avoiding for the foreseeable future.

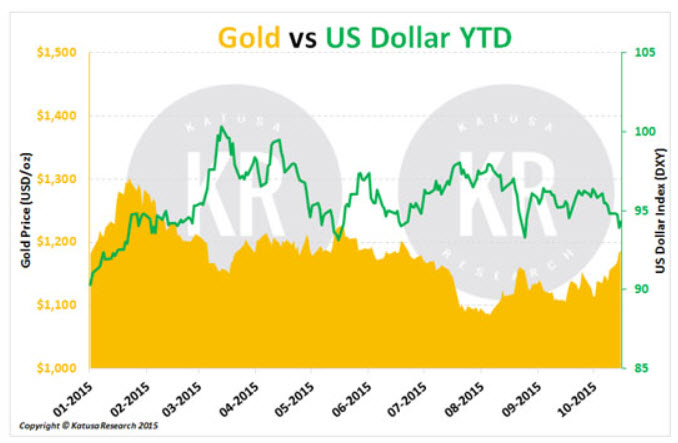

The Gold Report: You seem much more positive about gold right now than when we talked in June. Based on the chart you have on Katusa Research of the U.S. dollar versus gold and in the wake of the Federal Reserve's inaction at its last meeting, what's your thesis for gold for the rest of 2015?

Marin Katusa: As I said in the spring, I don't see the Fed raising rates this year. Using some simple game theory, for the Fed not to raise rates is the best decision. I still believe that. Gold has fared well compared to the price of the U.S. dollar, better than any other hard commodity. Gold is holding its own. The reality is, because the commodity markets are down, very little capital is being invested to replace the production of gold.

In the long run, I'm very bullish on gold. It's something I'm paying very close attention to through my fund. We've started writing checks on assets that I believe are very cheap and well priced in today's currency commodity markets and that I believe a major will want in its portfolio in a few years. Gold is the currency of kings and silver is the currency of gentlemen; it always has been, and always will be. When you see living legends such as Stanley Druckenmiller and well-known successful fund managers plowing hundreds of millions of dollars into gold, it's obvious gold is appealing at these prices.

TGR: Will the power of gold help the majors or the juniors more?

MK: I don't think the majority of juniors will take off until the majors take off, so watch the majors first. They will be the first ones to be repriced when gold really starts to take off. If a junior finds a world-class asset, it will rise based on its own success rather than on the strength of the market. We've seen many examples of that. But the producers will get the party started.

TGR: The majors are not all equal. What are some of the majors that you're watching that are doing a better job than the others?

MK: Balance sheet and debt risk is the first place to start. Also, consider whether a company has really written down all its crappy assets that it should. I know of a few companies that still haven't written assets that they should. Pay attention to the debt covenants. Everyone compares Goldcorp Inc. (G:TSX; GG:NYSE) to Barrick Gold Corp. (ABX:TSX; ABX:NYSE). But Goldcorp is in a much better situation than Barrick when it comes to the balance sheet and debt. The chairman of Goldcorp is a friend, so I'm biased and cheering for Goldcorp, but it's completely true regardless of my own bias.

"Newmarket Gold Inc. has been putting dollars into drilling and hitting very high-grade gold."

I like Goldcorp's assets better than Barrick's. Companies like Kinross Gold Corp. (K:TSX; KGC:NYSE) had a tough go because of its debt, high-risk assets and high cost to put in new production. Check the debt levels on these companies before you invest to determine if they would be able to survive the next two to three years in low commodity prices. At the end of the day, debt is the currency of slaves, so be very careful.

Investors looking at the top-tier companies also have to consider the royalty streaming companies, like Franco-Nevada Corp. (FNV:TSX; FNV:NYSE) and Silver Wheaton Corp. (SLW:TSX; SLW:NYSE). I would argue that they are in better shape than the producers themselves.

TGR: What about some of the midtier producers? Are there any you like in that category?

MK: In May, I was the first analyst to publish a research report on Newmarket Gold Inc. (NMI:TSX; NMKTF:OTCQX). That company has had a fantastic run. It has moved over 50% since then. This has been a great market for companies that are cashed up and have good assets. Similar to Canadian producers, Australian producers like Newmarket have the advantage of a devalued currency to make the selling price higher and the operating costs lower—using the currency crisis to their advantage.

TGR: Newmarket has been doing quite a bit of consolidating. Are you expecting more deals?

MK: Newmarket was an idea backed by some really good guys. CEO Doug Forster and Executive Vice President Blayne Johnson are backed by Lukas Lundin, Ian Telfer and Mike Vitton, and my fund is a big shareholder. Newmarket raised a bunch of cash and used that money to buy Crocodile Gold Corp. (CRK:TSX; CROCF:OTCQX), which was struggling. The Newmarket team took advantage of Crocodile's misfortune and increased production to over 200,000 ounces (200,000 oz) annually. In addition, Newmarket has been putting dollars into drilling and hitting very high-grade gold. It has been a nice win for all.

I think Newmarket will continue consolidating. For now, the near-term catalyst is to do more of what it's been doing. When the share price gets a bit higher, it will probably consolidate a near-term producer or a 100,000–150,000 oz annual gold producer.

TGR: What about the juniors? What are the juniors that you're watching?

MK: The first thing I look for is an excellent management team that is invested heavily in the company. Then I want to see if it owns a world-class asset. If this isn't an asset that a major would want to buy in a bad market, I avoid it. The world does not need another 400,000 oz gold deposit. A project has to be a game changer for a major.

TGR: What are some examples of the best people in the business?

MK: Ross Beaty, who after a number of successes is now focused on Alterra Power Corp. (AXY:TSX), has a great track record of delivering shareholder success, but more importantly, he's always the largest investor in his own deals. My fund and I are very large shareholders in two of Ross' companies. Alterra is an example of a stock that was significantly undervalued even though Ross Beaty and his team keep delivering great value. So I took a big position. Another one I like that Beaty is doing and nobody is paying attention to is Odin Mining & Exploration Ltd. (ODN:TSX.V). Beaty is quietly consolidating these world-class assets in Ecuador. It is super high risk but Beaty is definitely adding value, and I am a happy shareholder.

"Investors looking at the top-tier companies also have to consider the royalty streaming companies like Silver Wheaton Corp."

You cannot count out Robert Friedland with Ivanhoe Mines Ltd. (IVN:TSX). A lot of people are betting against him and his company. I've taken a large position in Ivanhoe in our fund. Those are two great examples of guys who are getting a discount in today's market but I believe will deliver significant success. For me, this is a dream come true market, as I can get proven management teams, such as Ross Beaty and Robert Friedland, at very low valuations.

TGR: What other companies fit the criteria?

MK: Midas Gold Corp. (MAX:TSX) is a fantastic project that I believe a major will eventually want to own. I am down on my position, but Midas has a solid management team, although they are promotionally challenged. It's suffering from two issues in this market: the permitting process—nobody cares about companies in that permitting period—and the capital cost to build the mine in this market is being frowned upon. A company like Osisko Gold Royalties Ltd. (OR:TSX) or Goldcorp will come up and buy that asset. Will it be this year or in three to four years? I don't know. But that asset is a past producer, very high grade and has over 5 million ounces of gold. That's why I've taken a large position. It has the right management team and the right project. It has the right type of geology in the right jurisdiction. That's a contrarian bet on gold. Most people are undervaluing it today, and that's when you want to buy. That doesn't mean it's not high risk. All junior resource speculations are high risk. That is why fortune favors the bold.

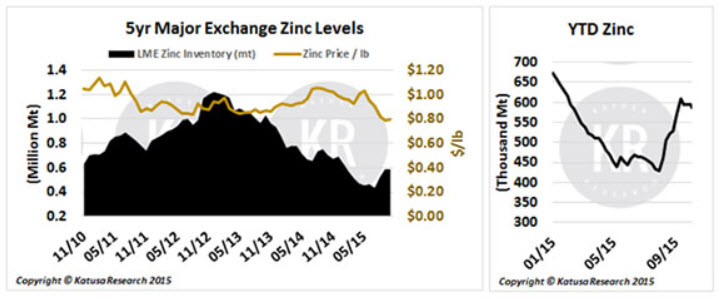

TGR: You also have an interesting chart comparing zinc inventories to price. How are you positioning yourself in that space?

MK: I'm just starting to focus on zinc. I'm not an expert by any means. Literally, outside of Ivanhoe, I have zero zinc exposure in our funds. So I haven't positioned myself in zinc. I just thought it was a very interesting data point to publish. Interestingly enough, many people have contacted me regarding the zinc chart, which tells me there are a lot of eyeballs on the sector.

TGR: You are one of the names along with Cambridge House putting on The Silver Summit & Resource Expo in San Francisco at the end of November. What do you hope people will come away with from this conference?

MK: The same thing that I'm hoping to come away with: deal flow to put my capital into the market and make money. There is no better place to meet management teams than a conference like this. You get to meet the Ross Beatys of the world, the man who built silver-producing mines through Pan American Silver Corp. (PAA:TSX; PAAS:NASDAQ). You get to ask questions of Silver Wheaton's management. These are the people who really understand the market. This will be one of the best conferences of its kind in the world with some of the most knowledgeable individuals in the resource sector present for you. All you have to do is make the effort of showing up. The beauty is that in a bear market, an average retail investor can spend time with key mining executives. I hope people at the show will walk the booths and ask questions.

One question I like to ask is, what other company would you invest in with the same type of market cap, sector and risk level as your own if you couldn't invest in your own company? That's a simple question that can really lead you to other opportunities. Plus, I will be there and you can ask me any question you want.

We have a fantastic line-up of fund managers and well-known market commentators, and you get to rub shoulders with people like Frank Curzio, Ross Beaty, Brent Cook and Grant Williams. These are fascinating, interesting people, and you get a chance to talk to them, learn from them and, hopefully, make money from the conference. That essentially is the point, to make money.

TGR: Thank you, Marin.

Marin Katusa is the author of the New York Times bestseller, "The Colder War." Over the last decade, he has become one of the most successful portfolio managers in the resource sector, such as his 2009 Fund Partnership (KC50 Fund LLC), which has outperformed the comparable index, the TSX.V by over 500% post fees. Katusa has been involved in raising more than $1 billion in financing for resource companies. He has visited over 400 resource projects in more than 100 countries. Katusa publishes his thoughts and research at www.katusaresearch.com.

DISCLOSURE:

1) JT Long conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report and The Life Sciences Report, and provides services to Streetwise Reports as an employee. She owns, or her family owns, shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: Silver Wheaton Corp. and Newmarket Gold Inc. Goldcorp Inc. and Franco-Nevada Corp. are not associated with Streetwise Reports. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

3) Marin Katusa: I own, or my family owns, or funds I am a shareholder in owns shares of the following companies mentioned in this interview: Midas Gold Corp., Ivanhoe Mines Ltd., Newmarket Gold Inc., Alterra Power Corp. and Odin Mining & Exploration Ltd. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.