Following a brutal two years for the Gold Miners Index (GDX), the sector has begun to perk up recently, advancing more than 20% off its lows to new 50-day highs.

This recovery can be attributed to the recent rally in gold back above the psychological $1,750/oz level and the fact that many miners had overshot to the downside during this bear market. In fact, many were trading at their most attractive valuations since 2018, when the gold price was hovering below $1,250/oz, and they were much less profitable.

Given the steep decline in the sector, several gold miners are trading at deep discounts to fair value.

In this update, we’ll look at two more attractive opportunities in the gold sector. Not only do these two companies have industry-leading growth profiles, but they have been beaten up sufficiently due to negative sentiment sector-wide that they’re offering considerable margins of safety at current levels.

Osisko Gold Royalties (OR)

Osisko Gold Royalties (OR) is a $2.33BB market cap royalty/streaming company in the gold sector, giving it a very low-risk business model. This is because the company generates revenue and cash flow from royalties and streams that it has purchased from developers and producers in exchange for helping them fund the construction or expansions of their projects/operations.

The result is that Osisko does not have to pay for sustaining capital to maintain these mines, it does not have to pay growth capital to expand these mines, and it is not subject to inflationary pressures if we see rising labor, fuel, explosives, or cyanide costs. Given this attractive business model, the company has reported year-to-date cash margins of 93% and 92% in its most recent quarter.

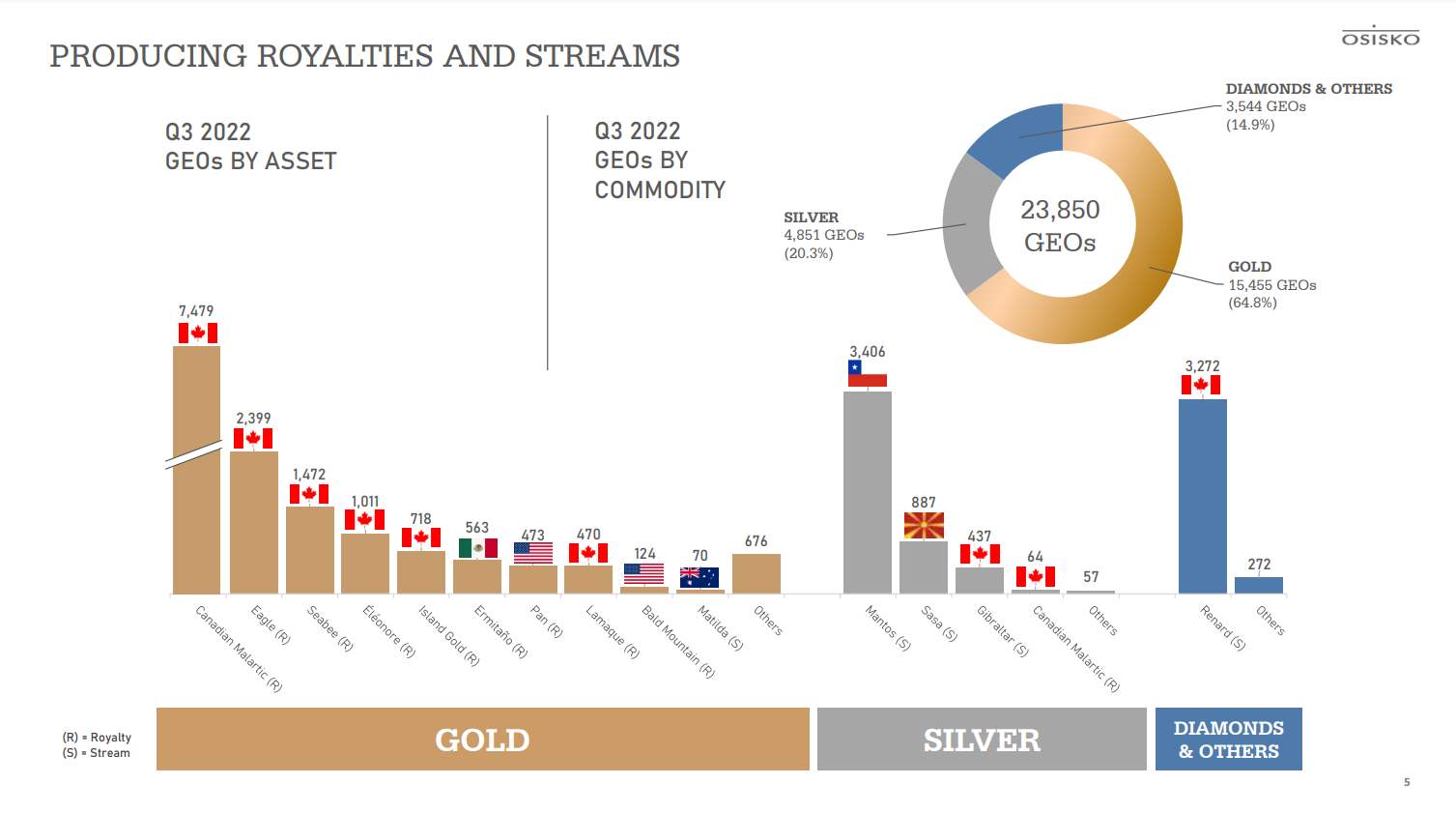

The other major advantage of this business model for Osisko is that the company benefits from meaningful diversification, receiving revenue from more than 20 different assets.

This translates to much lower risk than even the largest producers in the sector that have 10+ assets given that Osisko has less than 40% concentration to any one asset, meaning that if there’s a hiccup at one of its partner’s assets, there is limited impact on its quarterly cash flow.

However, Osisko further differentiates itself from its peers given that it has focused mostly on assets in the top-rated mined jurisdictions (Canada, United States, Australia), giving it low jurisdictional risk as well. I believe this should give the stock a premium multiple, but it hasn’t shown up in the valuation.

During the company’s most recent quarter, Osisko earned ~23,900 gold-equivalent ounces [GEOs], translating to revenue of $40.3MM and cash flow from operations of $38.3MM. This represented a 7% and 15% increase in revenue and cash flow from the year-ago period, despite a dip in gold/silver prices which was a minor headwind.

However, this growth is expected to continue in a major way over the next few years as Osisko benefits from multiple new assets coming online (Caribou, Windfall, San Antonio, Akasaba, Amalgamated Kirkland) and organic growth at existing royalty/streaming assets (Island Gold, Mantos, Eagle, Tintic).

Assuming things go as planned, Osisko could see its annual GEO sales increase from ~90,000 in FY2022 to more than 140,000 in FY2026.

Given the combination of an industry-leading growth profile, a mostly Tier-1 jurisdictional profile, and strong diversification (20+ paying assets and a portfolio of ~170 total royalties/streams), I believe Osisko can command a P/NAV multiple of 1.40, which is actually conservative relative to its larger peers at 1.60x - 2.10x P/NAV.

Based on an estimated net asset value of $2.3BB and 184MM shares, this 1.40x P/NAV multiple translates to a fair value of $17.50.

So, for investors looking for low-risk gold exposure, given that they can own one of the highest-margin names in the sector, I would view any weakness in OR as a buying opportunity, with over 40% upside to its conservative fair value.

Argonaut Gold (ARNGF)

Argonaut Gold (ARNGF) is a $220MM gold producer that has seen a significant fall from grace. In fact, the company briefly traded at a market cap of ~$800MM last year, near its peak, but its share price has since fallen over 90.

This has been attributed to significant share dilution and cost overruns at its Magino Project in Ontario. Unfortunately, due to the significant funding gap, the company was forced to take on additional debt and dilute shareholders by ~100% to ensure it could complete the project and bring its newest mine into construction, with the first gold pour expected in May 2023.

While this has certainly been a painful ride for existing shareholders, with over 500MM shares sold at depressed prices to fund the new ~$670MM capex bill (previously: ~$300MM projected capex), it’s created an opportunity for new investors.

This is because the company will have a much more attractive production profile beginning in Q2 2023 with a ~380,000-ounce production profile at ~$1,200/oz costs vs. ~240,000 ounces at $1,500/oz costs currently.

The other significant benefit is that this will improve Argonaut’s jurisdictional profile, reducing its exposure to Mexico, where it currently has three operations with this new mine in Canada.

Normally, I would avoid laggards and companies with a history of significant share dilution, and it’s typically best to avoid riskier stories in this sector.

However, with Argonaut trading at a market cap of $220MM and its Magino Project having an After-Tax NPV (5%) of $400MM even at a $1,725/oz gold price, investors are getting all of its other assets for free, and getting a significant portion of Magino’s current NPV (5%) for free.

This is especially true given that the operation is sized for much higher throughput rates than what’s currently contemplated (10,000 tonnes per day), and this NPV (5%) at Magino does not factor in the underground component of the project, which could easily add $100MM in value.

To summarize, this pullback in the stock has provided a fire sale, and I don’t recall the last time I saw sentiment this bad for a producer in years.

What’s the Best Course of Action?

Given the risk associated with buying a producer that’s still in the construction phase at its flagship project in an inflationary environment, I believe sizing conservatively is prudent.

That said, I see the stock as a steal at current prices for investors willing to step out on the risk curve, especially given that Argonaut has a new team in place that won’t be making the same mistakes as previous management. So, with the stock hovering near severely oversold levels, I have recently started a new position in the stock at US$0.265.

Investing in the gold sector is not without risk, but with the sector declining over 50% from its highs at its recent lows, there are several very attractive deals in the space.

In my view, Osisko Gold Royalties is a low-risk way to play for upside in the gold price with an industry-leading growth profile, and Argonaut is a way to get significant leverage to the gold price with higher risk but also a much higher reward.

Therefore, I see both stocks as Buys at current levels.

Disclosure: I am long OR, ARNGF

Taylor Dart

INO.com Contributor

Disclaimer: This article is the opinion of the contributor themselves. Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information in this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying small-cap precious metals stocks, position sizes should be limited to 5% or less of one's portfolio.