Those that subscribe to the efficient market hypothesis believe that there’s no edge or advantage when it comes to picking stocks. Thus, stock-picking is a binary event and boils down to a 50/50 probability or simply chance. Everything that can be possibly known about a stock is known, and all the available information, technical analysis, and fundamental analysis is priced into the underlying stock price. The efficient market theory may be the Achilles heel of professional money managers’ performance and their inability to outperform their benchmarks. A staggering 92% of actively managed funds do not outperform their benchmark hence the massive inflows into passive index investing and ETFs.

Furthermore, when looking at The Russell 3000 Index over a 26-year timeframe (1983 to 2006) which comprises the largest 3000 U.S. companies, 39% of stocks were unprofitable investments, 64% of stocks underperformed the Russell 3000 and 25% of stocks were responsible for all the market’s gains. Taken together, only 36% of stocks outperformed the Russell 3000 index. If the efficient market theory is correct, is stock picking a useless endeavor? If stock-picking boils down to chance, is there a strategy that places the statistical odds of success in one’s favor?

Efficient Market Hypothesis

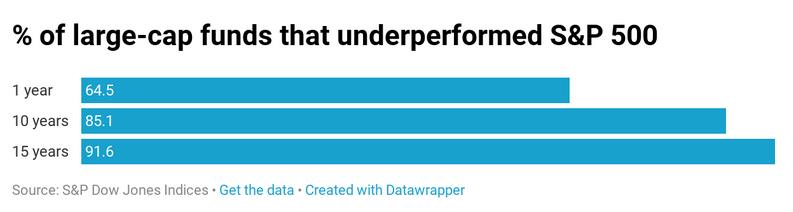

Markets aren’t always functioning efficiently. Markets can be irrational and become overbought or oversold. Outside of these extremes, however, markets are efficient, and over the long-term the vast majority of actively managed funds are unsuccessful at beating their benchmarks. Everything that can possibly be known about a stock is known, and there’s no edge in stock picking. As of Q1 2019, for the ninth consecutive year, the majority (64.5%) of large-cap funds lagged the S&P 500 last year. The longer the timeframe, the weaker the performance, after 10 years, 85% of large-cap funds underperformed the S&P 500, and after 15 years, nearly 92% are underperforming the index (Figures 1 and 2). These dismal results hold true across large-cap, mid-cap, and small-cap funds. Even if these actively managed funds happen to outperform their index, it’s due to chance, and this margin of outperformance is primarily negated by hefty management fees, rendering stock-picking useless. To further emphasize this point, for the Russell 3000, 39% of stocks were unprofitable investments, 64% of stocks underperformed the index, and 25% of stocks were responsible for all the market’s gains. Taken together, only 36% of stocks outperformed the Russell 3000 index.

{kind=link}