HealthEquity Inc. (HQY) was not immune to the market wide sell-off in equities during the fourth quarter of 2018 which disproportionally impacted growth stocks with high price-to-earnings multiples. The market quickly lost its appetite for these richly valued high-growth stocks with steep valuations. Health Equity’s rich valuation became a concern to me during the fourth quarter as its growth albeit double-digits, did not justify its sky-high valuation. This concern prompted me to write a piece discussing this concern and warned that the “current valuation is rich in an already frothy market thus caution at these levels is wise” prior to the stock selling off from $101 to $47 shedding 53% of its market value during the fourth quarter of 2018. The company continues to post quarter after quarter of double-digit growth in revenue and EPS without any debt on the balance sheet thus has been rewarded with a rich valuation as a function of its impressive growth and total addressable market. This high price-to-earnings multiple came under fire as the market moved into a risk-averse environment in the fourth quarter. As high-flying equities came down in the broader market sell-off, Health Equity lost over half of its market capitalization and erased all of its gains in 2018. Now that the market correction has passed and the company continues to post great quarterly growth along with enhancing its growth profile, the valuation is now compelling moving into its Q4 earnings and the stock is still well off its highs for a long-term investment.

Addressable Market and Market Position

On the fundamental level, the company is an intermediary servicing the secular growth Health Savings Account (HSA) space that’s largely independent of legislative actions, drug pricing, rising insurance costs while not playing any role in the pharmaceutical supply chain. The company manages funds allocated for medical, dental and vision expenses that are deducted on a pre-tax basis and deposited into a dedicated HSA account. The HSA space has grown in popularity as corporate adoption has allowed access to these plans in conjunction with consumer awareness.

HealthEquity currently manages $8.1 billion in assets across 4.0 million accounts against a potential market maturity of $1 trillion in assets across 50-60 million accounts. The durability of this growth has a long runway due to the secular growth in the HSA market. The company is sitting on largely untapped revenue sources where the vast majority of account holders have yet to invest any HSA money in investment offerings. Expanding margins for greater profitability is also unfolding as the older the account, the greater the gross margins. The company is currently sitting on a healthy balance sheet with $240 million in cash and cash equivalents with no debt. The company is posting accelerating revenue, cash flow, margin expansion and income growth with a strong balance sheet. I feel that HealthEquity will continue to post strong growth as it services the double-digit HSA growth market and manages more assets, accounts, and investments within these accounts. HealthEquity has demonstrated to be a great investment in the healthcare space that’s independent of the health insurances, pharmaceutical supply chain companies, drug makers or pharmacies.

HealthEquity’s Investor Presentation and Year-End Metrics

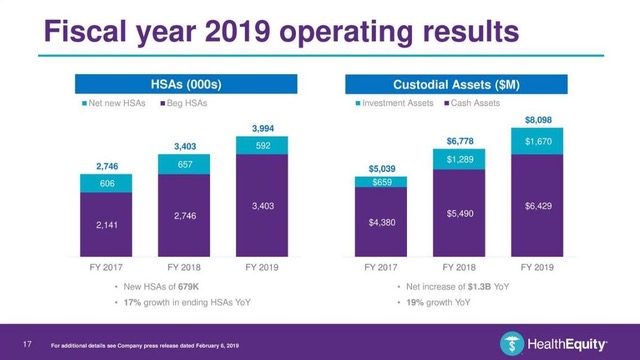

Recently, the company updated investors on its year-end metrics with total HSA members coming in at 4.0 million, an increase of 17% compared to Q4 FY18. Total custodial assets were $8.1 billion, an increase of 19% compared year-over-year (Figure 1).

Jon Kessler, President, and CEO of HealthEquity, “Excluding acquisitions, the team opened 674,000 new HSAs, a new record, helping our HSA Members add $1.3 billion in custodial assets during fiscal 2019. With more than $8 billion in custodial assets and 4 million HSA members, we believe HealthEquity has once again outpaced competitors and gained market share. The proprietary platform, remarkable purple service and unmatched ability to connect health and wealth position HealthEquity to lead the HSA market as it continues its strong, steady growth.”

96% of account holders have yet to invest any funds into investment offerings, potentially serving as a major growth driver as an untapped revenue source. We’re witnessing early adoption of this revenue source now that $1.67 billion is allocated in investment assets (Figure 2).

Figure 1 – Infographic depicting Health Equity’s big picture metrics

Figure 2 – HealthEquity’s growth across major business metrics

Future Growth and Healthcare Cost Containment Play

HealthEquity is one of the major players in the HSA secular growth market and has continued to gain market share over the years. The company currently has 15% and 14% market share in some accounts and custodial assets, respectively. HealthEquity has been growing market share with plenty of market expansion ahead of itself. Assuming a 15% penetration in both the number of accounts and assets, HealthEquity’s maturity may come in at 8.25 million accounts and $150 billion in custodial assets.

HSAs are becoming an invaluable option for consumers to contain medical costs and take control of healthcare spending. High Deductible Health Plans (HDHP) coupled with HSAs has contained family plan deductibles at a far lower level than any other healthcare plan. Additionally, funds deposited in the companion HSA account can be invested into mutual fund options to grow these funds over time. At age 65 these funds can be withdrawn without penalty at your effective rate, effectively serving as a second 401k over time. This dual-purpose account serves as a great means to contain healthcare costs while building wealth via investments over the long term.

Figure 3 – Cost containment play with HSAs as compared to other insurance options

Untapped Revenue Sources and Margin Expansion

HealthEquity is posting accelerating revenue, cash flow, and income growth. The company is sitting on untapped revenue sources and plenty of room for margin expansion. In terms of untapped revenue sources, of the 3.7 million members, 96% of account holders have yet to invest any money within its HSA accounts. This serves as an untapped pool of money that can be invested in various mutual funds while HealthEquity collects a small fraction of the dollar amounts invested in these investment accounts as management fees. Considering that the average age of an account is only 3.2 years and over 35% have been open for 2 years or less, this provides ample opportunity for future penetration in this investment space. Given the fact that these account balances are correlated with age translates into more probability that any surplus will be invested to drive account value further. As the company continues to grow, the float of HSA funds is expanding at a rapid clip year-over-year in a rising interest rate environment which only contributes to bottom line revenue to underpin the business.

Summary

Despite wiping out roughly 50% of its market capitalization in the Q4 market rout, HealthEquity has continued its path of accelerating revenue, cash flow and income growth across all segments of its business in the backdrop of an HSA secular growth market. HealthEquity looks compelling after this healthy correction as the long term narrative remains intact. The company is debt-free and expanding its balance sheet with just over $240 million in cash and cash equivalents. The company is sitting on untapped revenue sources, and gross margin expansion is beginning to bear fruit as accounts age and more funds are channeled into investment vehicles. HealthEquity is continuing to post strong growth as it expands the number of accounts, manages more custodial assets, expands gross margins and more accounts transitioning into investment vehicles. Furthermore, HSAs are serving as a dual purpose as a healthcare containment play offering more value than other insurance options while serving as a second 401k as assets can be withdrawn in retirement without plenty fueling the popularity of these accounts.

HealthEquity’s Fourth Quarter and Year-end Fiscal 2019 Conference Call Date: March 18, 2019

Noah Kiedrowski

INO.com Contributor

Disclosure: The author does not longer hold shares of HealthEquity. The author has no business relationship with any companies mentioned in this article. He is not a professional financial advisor or tax professional. This article reflects his own opinions. This article is not intended to be a recommendation to buy or sell any stock or ETF mentioned. Kiedrowski is an individual investor who analyzes investment strategies and disseminates analyses. Kiedrowski encourages all investors to conduct their own research and due diligence prior to investing. Please feel free to comment and provide feedback, the author values all responses. The author is the founder of stockoptionsdad.com a venue created to share investing ideas and strategies with an emphasis on options trading.