The S&P 500 slumped 19% in 2022, registering its biggest decline since 2008. Besides geopolitical turbulence and supply-chain disruptions, the market pullbacks were mostly driven by fears of a looming economic slowdown as an undesirable side-effect of the Federal Reserve’s fight against high inflation with aggressive interest rate hikes.

Since there is still a long way to go before inflation can be reined in to around the desired 2% mark, the central bank, by its own admission, is far from done with interest rate hikes. Hence, the market, subdued by the ever-increasing risk of a recession, is unlikely to stabilize anytime soon.

In fact, bearish sentiments have become so pervasive that the strengthening dollar has also been unable to offset the increasing luster of precious metals, such as gold. Such commodities are gaining popularity among market players as ballast during panic-driven market sell-offs and a time-tested hedge against a potential economic downturn.

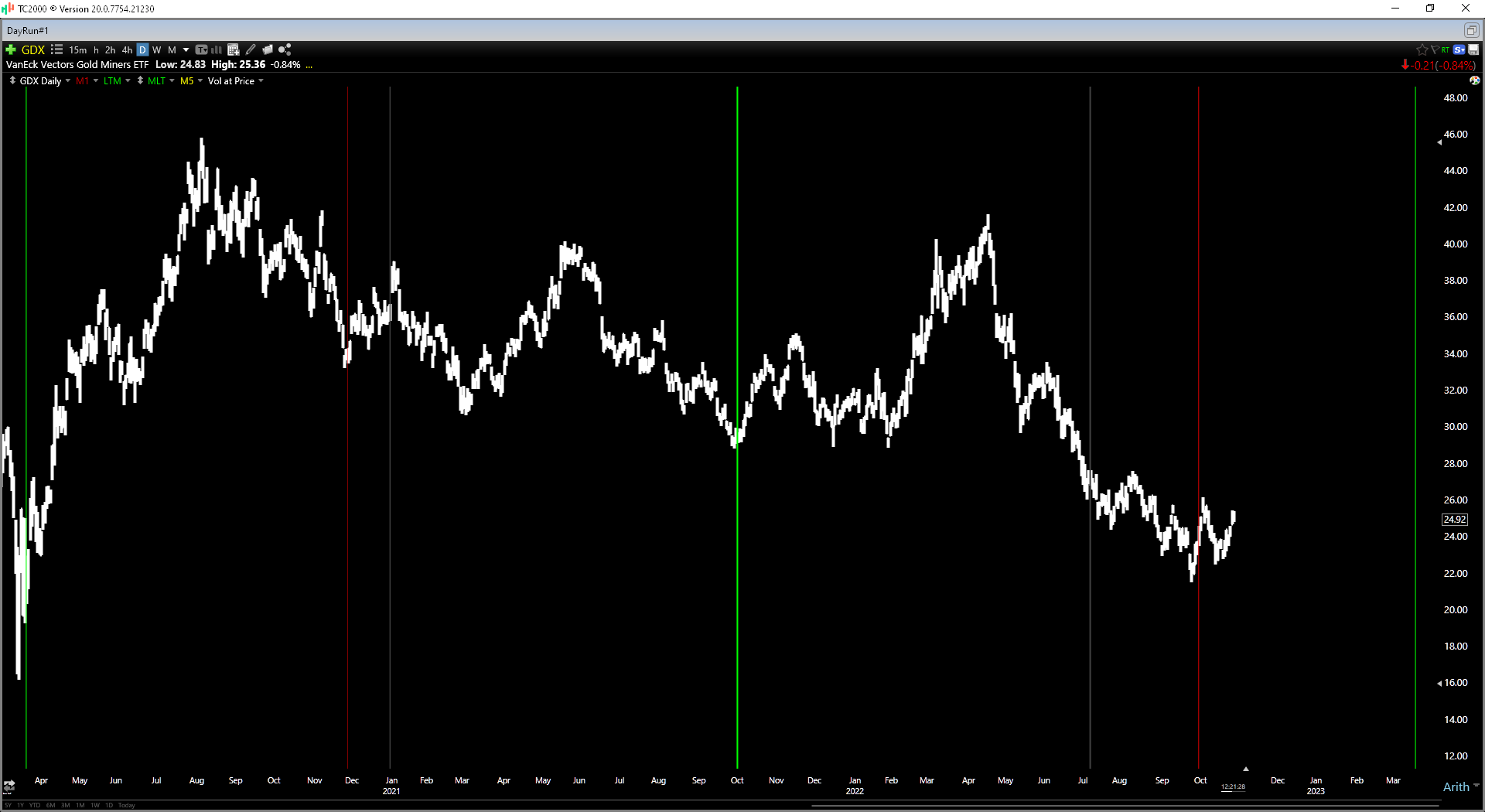

The VanEck Vectors Gold Miners ETF (GDX) is expected to offer downside protection. The fund is managed by Van Eck Associates Corporation. It offers exposure to some of the largest gold mining companies in the world.

Since gold mining stocks strongly correlate with prevailing gold prices, the ETF provides indirect exposure to gold prices.

Here are the factors that could influence GDX’s performance in the near term: Continue reading "Good Defense in a Bear Market"